For smaller, privately owned businesses, financing receivables may be the best or only option to maintain enough cash flow to continue to grow your business. Customers expect you, as a business, to provide them terms for repayment, which create accounts receivable for your business. Accounts receivable ties up your business cash until your customer pays it in full.

Two Options for Managing Cash Flow Needs

Supplies, inventory, payroll, initial contract start-up fees, and other expenditures can all be paid for using cash.

Alternatively, you can pay for expenditures using a line of credit (collateralized by accounts receivable) until your clients pay you. Once the bill has been paid, pay down the line of credit so that it may be used for the next project.

Managing Working Capital

Working capital is another area to pay attention to if you want to keep growing. Working capital helps you keep your business viable by covering day-to-day expenses, funding larger initiatives, allowing you to buy more inventory, and keeping you afloat through the toughest periods, such as the economic slump.

The money you have on hand, whether profit-savings, a bank loan, or other means of raising capital, is your working capital. Working capital funds your day-to-day operations, helps you pay rent and staff, and covers other operating expenses.

Calculating the gap between current assets and current liabilities on your balance sheet—net cash flow—is a straightforward calculation. This metric assesses your company’s liquidity, capacity to satisfy short-term obligations, and ability to fund day-to-day operations.

It is also common in a small business that the owner will inject his own cash to pay the suppliers. Financial institutions have come up with different products, also known as working capital loans, to solve this problem and help businesses generate additional liquidity to finance their working capital gap.

Types of Financing

Let’s look at the two most common kinds of traditional financing: term loans and lines of credit. Both look at a company’s credit history and score when deciding on loan alternatives to help with cash flow and business expansion.

Term Loans

Term loans may have larger borrowing limits and longer payback periods than other types of loans, making them a better option for funding. When the amount of days necessary to transform inventory into completed items and collect the cash from a sale drains day-to-day operational cash, a demand for working capital term loans may develop.

Short-term loans can have a repayment plan that corresponds to the product’s sale or, in some circumstances, a longer-term permanent working capital injection to help a firm reach its full potential.

Lines of Credit

A line of credit, similar to a credit card, is a pool of accessible funds from which you can borrow as needed. After you’ve been authorized, you may spend the money, but you don’t have to borrow it or pay interest until you actually use it.

Lines of credit help your company’s cash flow by covering costs while you wait for payments from customers (receivables) or cash sales. In order for the firm to develop, it should sell more items on a long-term basis. However, while your spending may remain pretty constant from month to month, your cash flow may fluctuate. A cash reserve of 6-12 months’ worth of costs is a good rule of thumb for every firm.

Keep in mind that, due to interest, financing might be more expensive in the long run than paying cash, so study the terms and conditions carefully, including any prepayment penalties on loans.

Statement of Cash Flow Needs

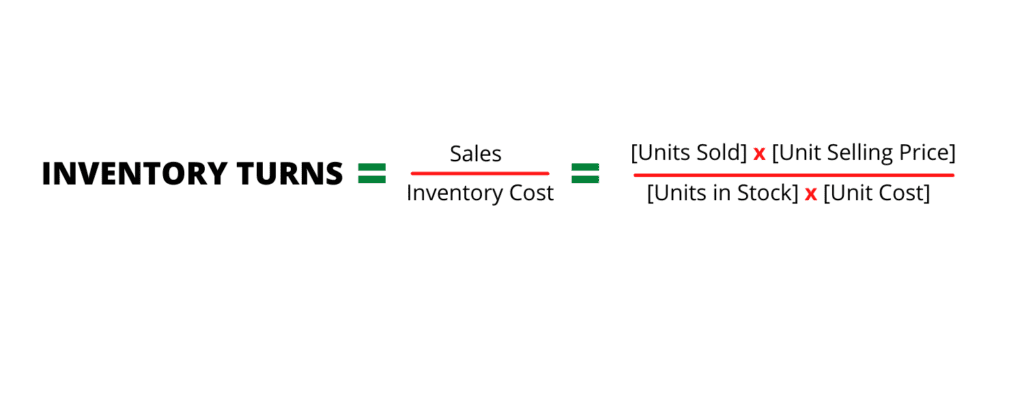

The rate at which you replace your inventory in a particular period of sales is known as inventory turnover. In a nutshell, it’s a metric for determining how successfully a firm produces sales from inventories. Use this easy calculation to determine your inventory turnover:

Having a high turnover ratio means that you are doing well getting payment on accounts. This means that you have good cash flow.

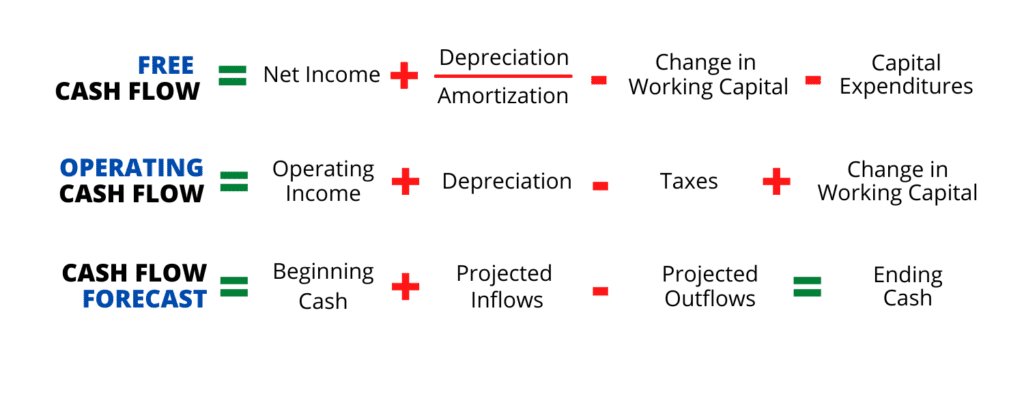

To assess how much you need to adjust your inventory or negotiate for better inventory financing, review your statement of cash flow. Here are three cash flow formulas that you can use to calculate current cash flow (Operating Cash Flow), available cash (Free Cash Flow), and future cash flow needs (Cash Flow Forecast).

Smart Management of Cash Flow

You can negotiate terms or rates on your accounts payables as a small business owner. Be proactive when engaging with your vendors to assist you manage your cash flow and enhance your present operations and inventory management, whether it’s due to seasonal fluctuations in sales or recovery from the pandemic last year.

Make a plan first of exactly what you will speak to your vendor about and what your “ask” will be, as well as making a cash flow projection of what you expect to save, delay, or improve. A cash flow projection can also serve as a marker or warning system before you run into trouble with vendors. Even changing the due date of a payment to another date of the month, say 15th instead of on the 1st, may help manage your cash flow and inventory purchases better. Look out for opportunities to negotiate a rate if you are approached by a competitor.

Make sure there’s a clear accounts payable (money you owe others) and accounts receivable (money you owe yourself) procedure and reporting system in place, and that everyone on the team is working toward the same objective of maximizing cash flow and minimizing working capital.

One approach is to extend account payables as long as possible, but doing the opposite and paying early may lead to added benefits or discounts with vendors. Don’t sacrifice your supplier relationship by delaying payment, but rather speak to them to rearrange payment schedules or negotiate a better rate for paying early or in advance.

Additionally, go paperless as much as possible to guarantee efficiency and the opportunity for team members to readily exchange and evaluate reports.

In the case of accounts receivables, if you’re short on cash, try providing your customers a discount if they pay early. You may speed up payment by giving a discount on the invoice, which you must expressly specify, because sending out invoices offers your clients a 30- or 60-day payment window.

- For example, 4/10, Net 30 would mean the customer would receive a 4% discount if they pay their invoice within 10 days as opposed to 30.

- Another example would be 2/15, Net 45, which offers a 2% discount if paid within 15 days of an invoice with a 45 day due date.

Calculate your normal profit margin to determine an appropriate percentage discount to offer by paying early.

There When You Need Us

Contact one of our business bankers today to discuss your business financing options.